This article is an introduction into Blockchain

Technology, explaining the basics of Blockchains on

the example of Bitcoin. It gives an overview over

the challenges Bitcoin tried to solve and

illustrates the novel approach Bitcoin chose to

create a peer-to-peer payment solution. As the first

public and permissionless Blockchain, Bitcoin laid

the foundations of projects that followed in the

years after its launch, such as Ethereum for

example. Grasping the core concepts behind Bitcoin

provides thus a great base for understanding

Blockchains in general as well as more recent

Blockchain projects and to grasp the differences to

the Bitcoin implementation.

Posted: 06 May 2022

Introduction

The idea behind Bitcoin was made public in a whitepaper released in 2008, by a certain Satoshi Nakamoto. Until

today, the identity of the author of this paper remains unknown

and there exist more than a few speculations on who and where

Satoshi is.

This article however, is about the principles behind

Bitcoin, as they are described in the whitepaper, and

the actual implementation of the Bitcoin protocol. The

latter fuels the Bitcoin Blockchain, which has been live

since early 2009.

Bitcoin marks the first public and

permissionless

Blockchain network. Since 2009, a vast ecosystem of Blockchains

has emerged, with new projects joining the space every day.

But to understand how we got there, one should start with

Bitcoin. This is how this article is structured: It starts

with a closer look at the ideas and previously attempted

solutions that drove the conception of Bitcoin as a peer-to-peer

payment system. It follows a quick discussion about privacy

on the Bitcoin network and lastly, deeper insights will be

given into how the consensus mechanism, the much discussed

*Proof of Work* algorithm, works in the case of Bitcoin.

Core Idea

The core idea of Bitcoin is to remove any middleman from

a digital payment system. This is to say: digital

transactions would be sent directly from someone taking

part in the network to someone else, without a middleman

verifying the transactions or settling conflicts. This

is of course meant to strip this party in the middle of

any power it might possess, such as reverting

transactions for example.

However, just removing the bank will inevitably lead to

problems. Consider the following digital payment system:

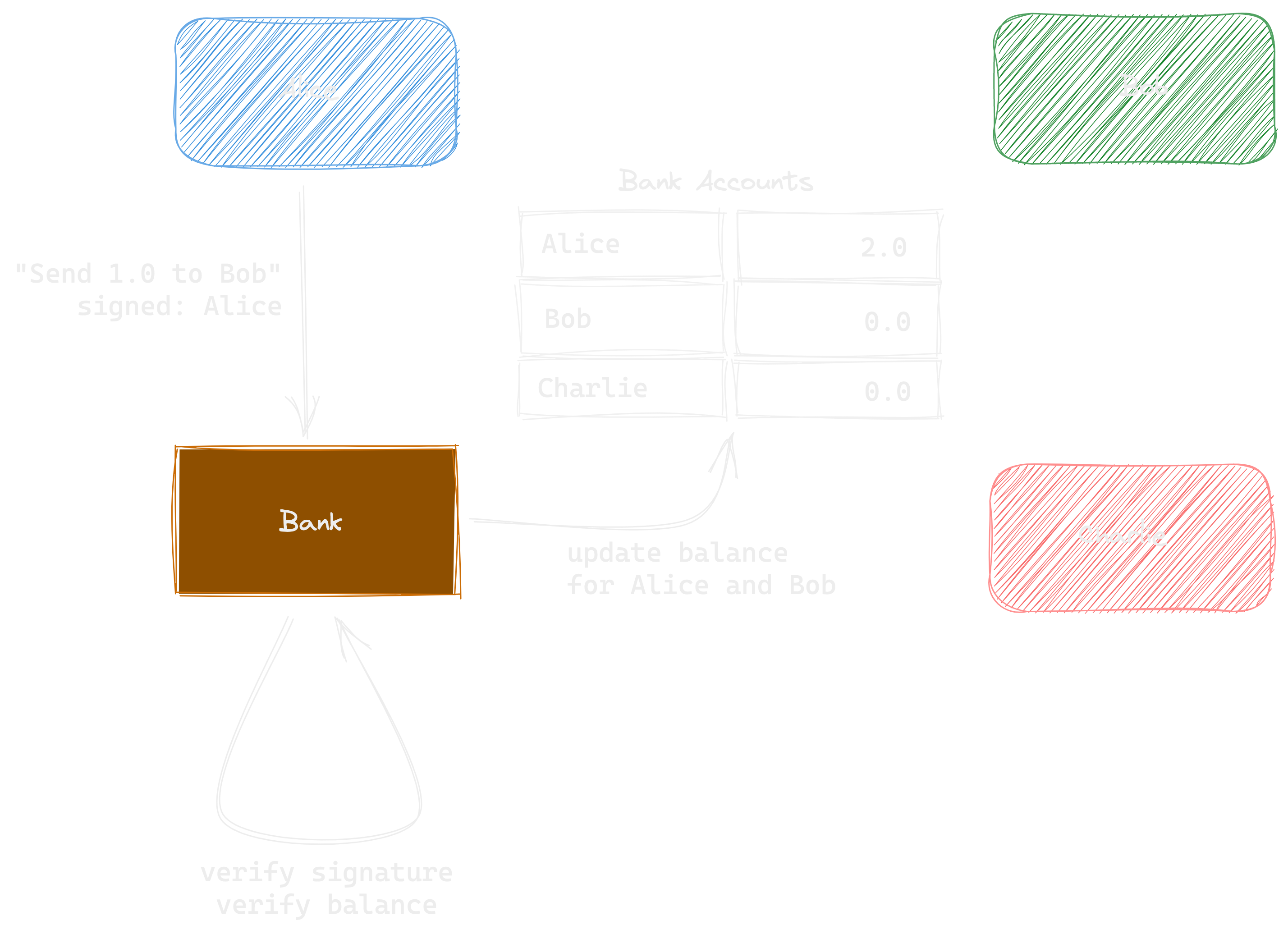

Three participants, Alice, Bob and Charlie, can send

each other digital money through a bank.

The bank holds all account information and is as such

able to verify transactions. If Alice were to send $1.0$

coins to Bob, she would have to digitally sign a

transaction, and send it to the bank. The bank in turn

would verify the signature as well as Alice's account

balance to make sure she has sufficient funds to execute

the transaction. If those conditions are met, the

account balances of both Alice and Bob will be updated

accordingly.

The Intermediary

The problem with the intermediary, in the philosophy of

Bitcoin where one should not trust any third party, is

first of all that it holds and manipulates all the

balances as a monopoly. As such it can refuse

transactions and generate money at will. Banks are

certainly regulated but they may nonetheless change your

account balance. What is more, as a single point of

failure in the system, the bank processes all

transactions. If it were to fail, the other participants

in this network, Alice, Bob and Charlie, would not be

able to send money to each other.

Remove the Bank

In light of the problems described above, it is rather

natural to try and solve the problems by just removing

the bank. In this hypothetical system without a bank,

every participant in the network would have to hold a

copy of all accounts and their respective balances to be

able to verify transactions.

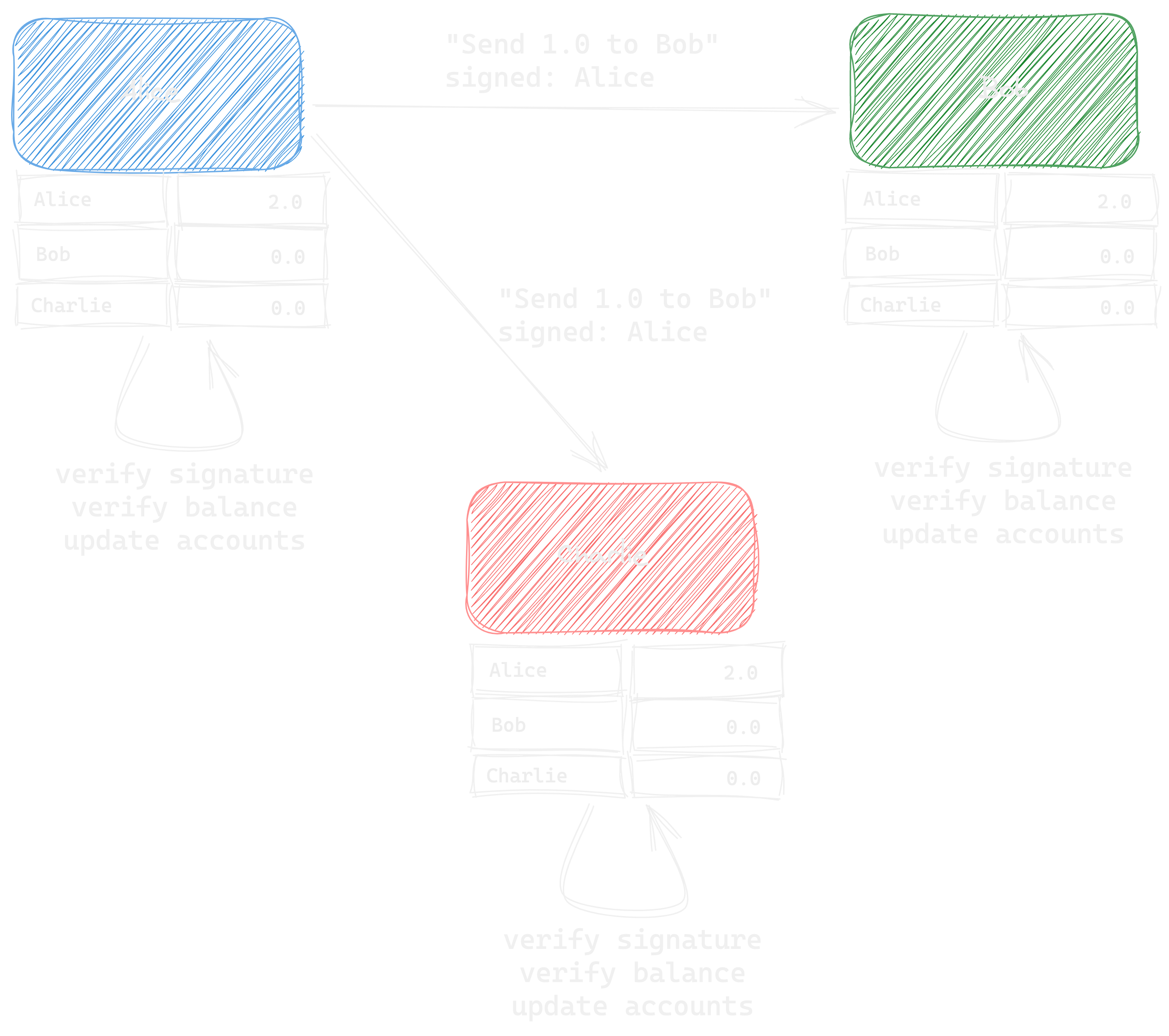

If Alice were to send the same transaction as in the

previous example, she would send a message to all

participants this time, including the amount she wants

to send as well as her digital signature. All parties

would verify the transaction according to their copy of

the account balances as well as the validity of the

signature and update the balances accordingly.

With everyone having updated their copy of the account

balances the same way, thus agreeing on the change the

transaction initiated, the network reached Consensus. This is essential for the system to work, consensus

amongst the participants has to be achieved.

Cheating the System

What would happen if Charlie tried to cheat the system

by increasing his account balance in his own copy of the

accounts by one coin and then sending one coin to Alice?

When verifying the validity of the transaction, Alice

and Bob would fail to verify that Charlie has the needed

amount and simply refuse to update the balances, even if

Charlie's signature was valid.

Thanks to the majority of the network agreeing on not accepting

such transactions, this fraudulent activity would be without

effect. It becomes more complicated if the majority were

to be malicious.

A way to break this simple system, is to perform what is

called a Replay Attack. Imagine Bob

copies the message Alice just sent (sending 1.0 coins to

Bob), and sends it to Charlie including a copy of

Alice's signature. Charlies would deem both signature

and balance valid and perform an update of the account

balances. Now both Bob and Charlie increased the amount

of coins held by Bob, thus representing the majority of

the network. Alice cannot counter this attack with the

simple rules of our system.

Serial Numbers and Transactions

A common concept introduced at this point are Serial Numbers. That is, numbering each coin and including the serial

number of the coin which is subject of a transaction in

the transaction message. In this case Bob would have to

modify the message and include a serial number of a

different coin Alice is currently holding. This

modification would make the signature on the transaction

invalid.

However, consider this: Alice could after some time come

back into possession of the same coin she sent earlier

with the transaction Bob has copied. Bob could wait for

that moment and then send the transaction again, keeping

a valid signature since he did not change the

transaction message.

And this is where Bitcoin introduces an intriguing and

novel concept: Transactions. By replacing the notion of Coins

with Transactions, the account balances

are no longer stored as the number of coins (with or

without Serial Numbers) someone owns, but as the sum of

the values of in- and outgoing transactions on that

account. It takes some time to wrap one's head around

it, but the advantage of offering protection against

Replay Attacks can be seen immediately: a transaction

holds basically the history of transacted amounts.

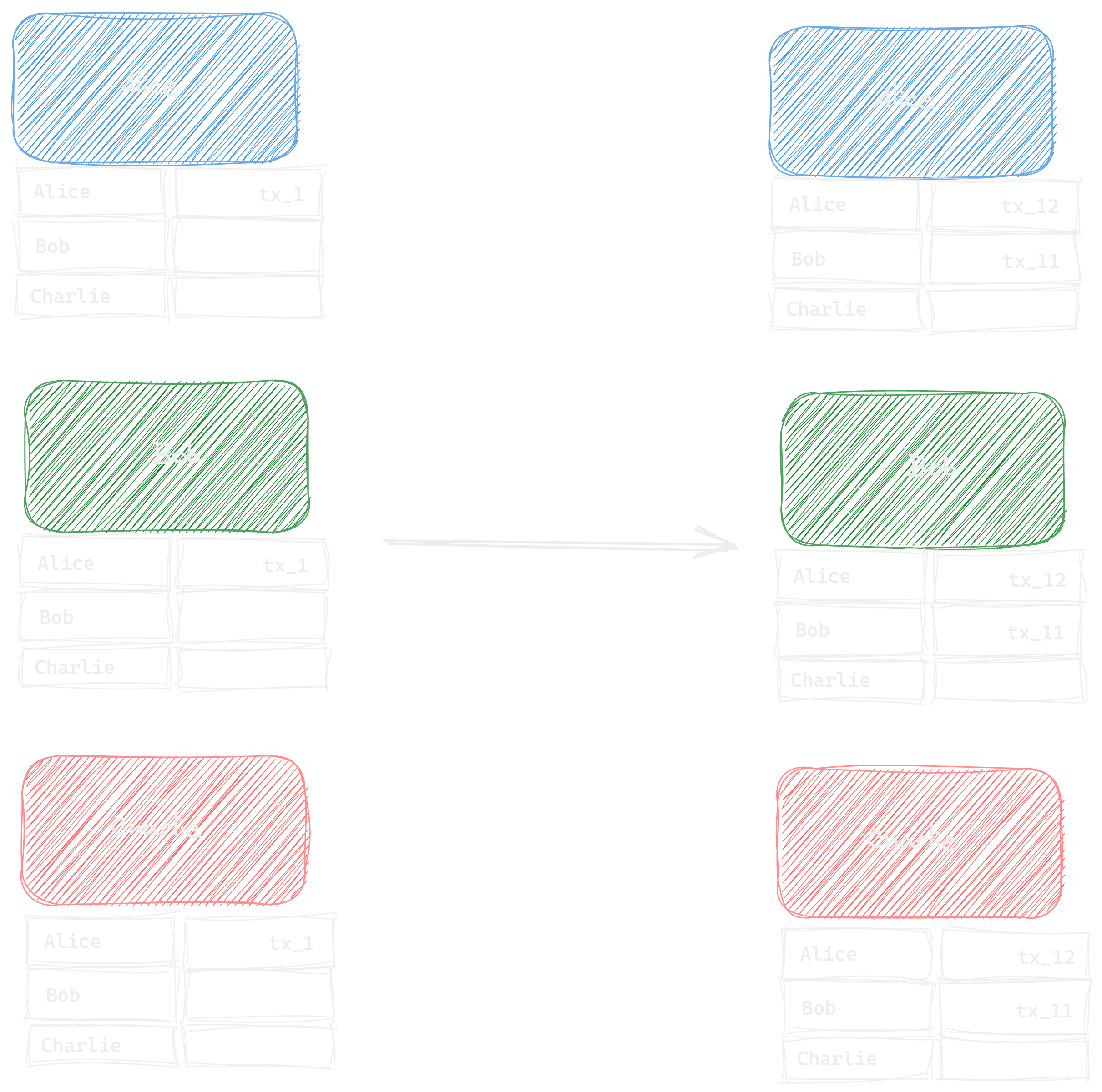

Consider the following example: Alice sends an amount of

$1.0$ coins to Bob. However, this time she sends a

transaction, named $tx_{11}$, which is the result of

$tx_1$, which points at Alice's account, transacting

$2.0$ coins to her. Transactions are conceptually made

of incoming transactions, and outgoing transactions,

where the sums of both have to be equal. In our case,

$tx_1$ had a value of $2.0$ coins associated with it. So

in order to match incoming and outgoing value, *$2$*

transactions will be created, one with $1.0$ coins

pointing towards Bob's account ($tx_{11}$) and another

one with $1.0$ coins pointing back to Alice's account

$tx_{12}$. The latter one basically represents the

change Alice is getting back.

Alice would broadcast the transaction to both Bob and

Charlie. They would in turn verify that transactions

with a sufficient amount point to Alice's account and

check if the signature is valid.

The following figure illustrates the network before and

after the transaction was sent and verified by the

participants.

To come back to the Replay Attack: Bob would now not be

able to send the same transaction again, since the whole

message of the transaction has changed and continues to

change on every transfer.

Double Spending

Up until this point, reasonable solutions existed before

Bitcoin that would prevent the aforementioned problems.

One challenge that remained unsolved was the protection

against Double Spending Attacks.

The following scenario illustrates such an attack. Alice

sends a transaction with amount $1.0$ coins to Bob and

at the same time a transaction with the same amount to

Charlie. If she sends the message about the first

transaction to Bob and another message about the second

transaction at the same time to Charlie, both appear

valid to the respective receivers. In this case both

would update their account balances and Alice would have

spent the same amount twice, while only paying once.

This obviously leaves the network in a state without

consensus.

To prevent double spending attacks, Bitcoin uses Public Announcements.

Public Announcements

The idea behind public announcements is simple:

broadcast any transaction to everyone on the network.

Meaning, you cannot select who will be the receiver of

your transaction. In Bitcoin this results in a pool of

unapproved transactions, where all broadcasted

transactions are collected.

A random network participant will be selected to

validate a transaction and send it to everyone else, so

they can update their local copy of the accounts.

Sybil Attack

This random peer selection has one problem: if we were

to choose all participants with the same probability,

someone could use multiple connections to the network to

be more often the selected participant to validate

transactions. This would enable them to favor their own

transactions for example. The described scenario is

called a Sybil Attack.

The key to solving this problem lies in the mechanism to

select the network participant who is to announce the

next validated transaction. Bitcoin introduces a

mechanism called Proof of Work,

implementing a selection based on computing power with

some random elements to keep the selection fair.

Although it does not render Sybil Attacks impossible, it

makes them at least sufficiently difficult to discourage

this kind of attack.

Proof of Work

To become the peer that is able to publish the next

validated transactions, all participants compete in

solving a cryptographic challenge. First, they collect

transactions from the pool of publicly announced

transactions. Then, they all try to solve a problem,

using the Proof of Work algorithm. Whoever si to find

the solution first, can announce the transactions. All

other peers can verify the solution to the challenge and

the transactions that are being broadcasted, which is

inherently less computationally intense as computing the

solution itself. Lasty, everyone can update their copy

of the transaction history.

The process described above deals in batches of

transactions. In the context of Blockchains, this is

described as the basic unit of a block.

Meaning that every time someone publishes new approved

transactions and a challenge solution, they effectively

publish a block. All blocks are linked to their

predecessors, in a way that modifying the order is

virtually impossible. This also serves as a means to

keep the transaction history clear, since accounts only

store transactions, not coins.

To do so, a block contains a Hash of the previous block

besides the transactions and the Nonce, which represents

the solution to the challenge.

In case two peers find the solution at the same time,

the chain splits, since both blocks are valid and are

linked to the latest block on the chain. For the next

block, peers can decide on which end of the chain they

want to work on in order to extend it. The general rule

is to work on the *longest* chain of blocks. As a

result, as soon as a new block is added to either of the

two blocks (without a 'competing' block at the same

time), this chain effectively becomes the longest chain

and all peers start to work on extending it.

Blockchain

The previous paragraph introduced the blockchain. It

represents a digital ledger, holding information about

all accounts and the transactions that point at those

accounts as last recipients. As such, it is possible to

verify a chain of transactions from the first ever

transaction to its current endpoint.

Another interesting property of this network is that

peers, called nodes, can drop in and out of the network

at any time without compromising its functionality. As

soon as they join again, they update their information

about the current state of the ledger and fetch pending

transactions. Then they start working on the longest

chain.

There is however, a possible attack that remains: a 51%

attack. This describes an attack where one party or

multiple collaborating parties possess more than 51% of

the computing power on the network. This would make it

more likely that a member of this malicious group

becomes the node that appends the next block, and would

thus be able to act maliciously.

To mitigate this risk, Bitcoin introduces incentives for

nodes solving the challenge, so called miners, to remain

neutral. Miners collect transaction fees from the

transactions they include in their blocks, making it

profitable to add blocks to the chain and behave. On top

of that, every new block (up until a certain point in

time), creates one transaction that sends a certain

amount directly to the miners account as a reward for

mining the block.

Thus, it becomes not only infeasible, but also

unprofitable to attack the network, since that would

also destroy the value the miners are receiving.

However, what makes the network inherently safe, is a

high number of miners. The more miners and ,more

importantly, the more decentralized the computing power,

the safer the network from 51% attacks.

Mining

Mining, as introduced above, is an essential part of

Bitcoin. And although often described as a

'cryptographic challenge' or a 'mathematical puzzle', it

really is all about brute force and luck.

The basic idea of the Proof of Work algorithm is the

following: before publishing a new block, one has to do

some kind of computation that requires computational

resources. Although this mechanism got popular with the

emergence of Bitcoin, it has been invented as a

protection against spam. Instead of being able to send

requests or emails for example immediately, the sender

has to use computing power and attach a proof that they

did the work to the message, only then it will be

treated. When sending one email or request, this

represents a negligible overhead. However, if you want

to generate thousands of those requests, it will require

massive computing power to send them all at the same

time.

Hash Function

The most important part of the algorithm is Hashing. A hash can be computed over any input, whether it is

a simple number or a file. The output of a hashing

function, the actual hash, is always of the same length,

no matter the input. Bitcoin for example uses a hashing

algorithm with a 256 bit output, which accordingly

outputs a number between $0$ and $2^{256}$.

Hashing functions have very interesting properties. For

one, they are *one-way* functions, meaning any input can

create a hash value as output, but it is not possible,

or at least not feasible to compute the input with a

given output. Moreover, a hash function should be collision free. That is to say, the function will never create

identical outputs for different inputs. These properties

are key in understanding why hashing functions are being

used in cryptography.

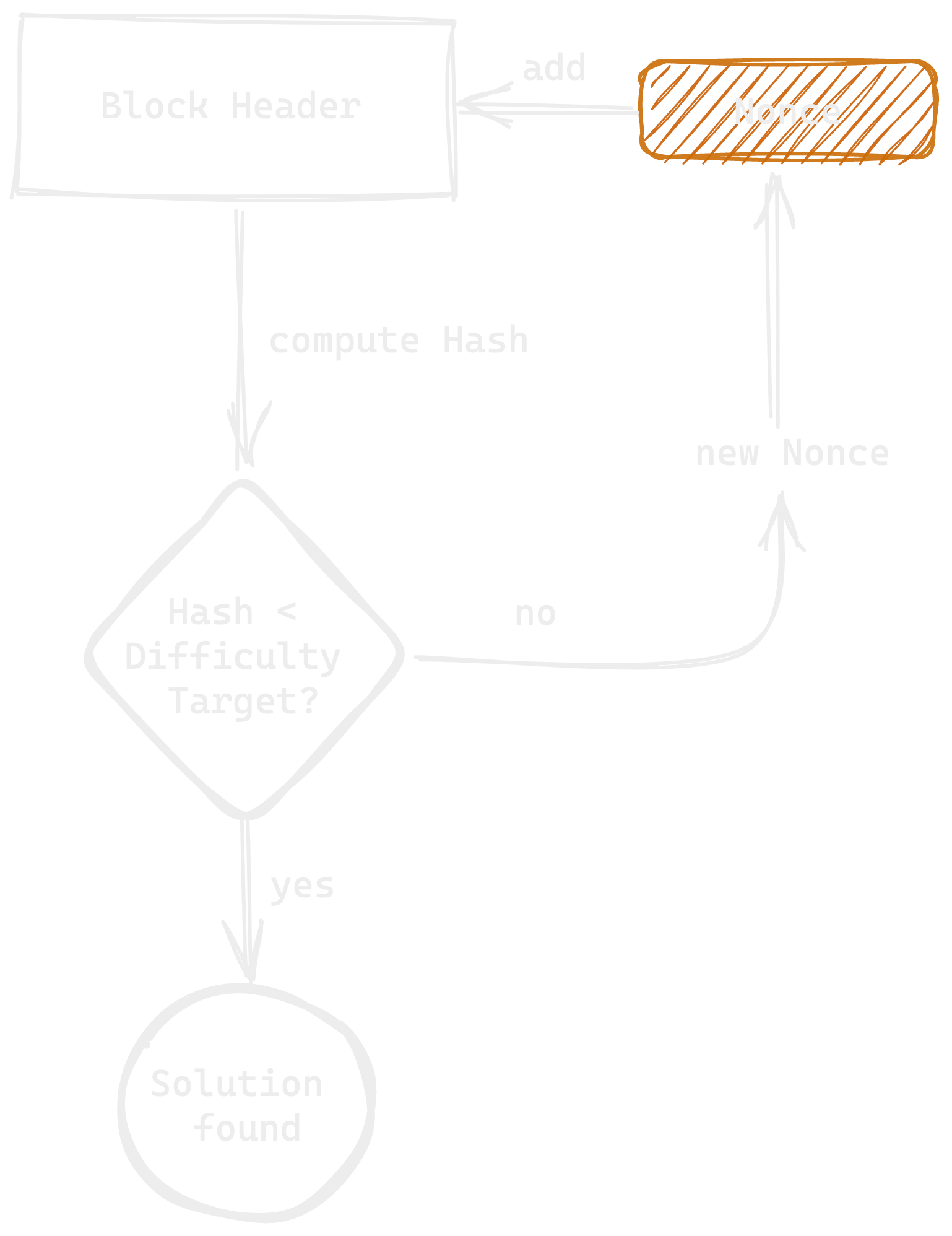

Bitcoins Proof of Work Algorithm

In the case of Bitcoins Proof of Work algorithm, the

mining software computes a Hash using the data contained

in the header of the block the miner wishes to add to

the chain. The header of a block holds information such

as the hash of the previous block, information on the

transactions included and a Nonce.

While most of the data in the header is fixed, the nonce

can be changed by the miner. This variation produces

different Hashes as output.

The output hash is then compared to a given value, which

represents the difficulty target of the problem. If the

computed hash is lower than the difficulty

target, the problem is solved and the miner may publish the

block. However, if the number exceeds the difficulty target,

the miner will have to retry, by changing the nonce and recomputing

the hash. This process is being illustrated by the figure

below.

When comparing computing power for miners, the most

important number is how many hashes per second the

machine is able to compute. Since, the more hashes you

try, the more likely you are to find a hash solving the

problem.

The difficulty of this algorithm, i.e. the average time

it takes to find a solution, can be guided by the value

of the difficulty target. The higher the target value,

the 'easier' it is to find a solution, since more hashes

satisfy the condition $Hash lt target$. The Bitcoin

protocol aims to maintain an average Block time

of 10 minutes. In order to achieve this, the difficulty is

being automatically adjusted every 2016 blocks (roughly 2

weeks), with regards to the current total

Hash Power of the network. The Hash Power

indicates how many hashes can be computed by all miners combined.

Since the output of the hash function cannot be

predicted, small miners, with little computing power,

also stand a chance in solving the problem through pure

luck. This incentivises users to join the network as

miners, even without a super computer.

Privacy

To round this article off, a quick note on privacy in

the Bitcoin network. Bitcoin itself does not grant you

full anonymity. This is due to how transactions are

being stored: visible to anyone on a public ledger. What

keeps you private is the fact that the sender and

recipient of a transactions are represented as a row of

numbers, addresses. This address is

associated with all transactions you receive and send

from a given wallet. As soon as someone is able to

associate a given address with a name, they are able to

trace all transactions ever made by that address.

It is of course hard to trace transactions, especially

if someone is to employ techniques of obfuscation, such

as using mixers for example. However, there is no

guaranteed privacy through the Bitcoin protocol.

This marks the end of this introduction into Blockchain

technology. If this catched your interest, there are

lots of topics to explore from here: Privacy,

Smart Contracts,

Decentralized Autonomous Organizations

and Stablecoins, to name just a few (feel free to use these

links to get down into the rabbit hole).